Protecting your Wealth and Building Strategies for Retirement Income

Here's How We Do It

Sound Financial Planning begins with your goals and priorities in mind. Once those items are clear, and if we can gain an understanding of market volatility, the risks of investing in different strategies, and the value of an investment plan that is aligned with your unique investment profile, then investing with confidence becomes easy.

Ryan Olson, CFP®, MBA

President · Founder

WealthCheck is designed for employees with stock options and soon to be retirees.

The WealthCheck Process for Equity Compensation and Retirement Income

Step 1: Gather the facts about your current situation & clarify your goals.

Step 2: We analyze your current balance sheet, seeking opportunities to lower taxes, and optimize your investment plan.

Step 3: We implement your plan with time tested systems, portfolios to meet your investment needs, and asset protection strategies that seek to diversify and protect you and your family.

When you’re finished with this process, you’ll have a clear and concise view of your financial life. Your WealthCheck Plan will provide you with potential tax savings strategies, a clear view of your stock options, with a path toward diversification. For retirees, your plan will show you how you can take withdrawals from your retirement savings, giving you the best chance for making your money last as long as you do.

Equity compensation poses tremendous opportunity, and also significant pitfalls if not well planned for.

Our WealthCheck Process will identify:

- How to optimize your equity compensation

- Minimize tax impact

- Diversify your holdings

Soon to be and new Retirees, how to take a steady income from your retirement savings and manage the ups and downs of the stock market:

Our WealthCheck Process will:

- Identify the appropriate amount of income to pull from your retirement accounts, with your long term goals in mind.

- Minimize the tax impact of withdrawals

- Diversify your holdings

Call our office (805) 439-3800 or email us here: coby@mustangprivatewealth.com

For our initial meeting, gather any and all financial related documents, including the following:

- Equity Compensation Documents: Employment Contract, Stock Option Subscription Documents with Vesting Information

- 401k, 403b, 457, IRA, Roth Account Statements

- Bank Statements

- Mortgage Statements

- Recent Tax Returns

- Investment Account Statements

- Insurance Policies or statements

The WealthCheck™ Process

Determine Your “WealthStage”

Your WealthStage is determined by several variables, most notably your time horizon and unique investment profile combine with your age and investment goal to determine which stage you’re in.

The WealthStages:

Pre-Earner (grade school to college/post-graduate education)

The pre-earner stage is the time when grand-parents and parents instill family values and financial education to their family/younger generation. College Saving and UTMA strategies, when

appropriate are often employed for clients in this stage.

New-Earner (Fresh college grad/trade school new career)

This is the stage when serious saving and budgeting needs to occur. Taking time to understand your your paycheck, save, pay off loans, develop credit, buy a home are the foundation for future financial success. In this stage we spend time educating about financial markets, the power of compounding interest, and the importance of tax efficient investing. Also, we talk about planning for the financial burden having a family might have on one’s life. Learning about the various insurance coverages begins in this stage.

Mature Earner (Set career path and peak earning years)

In this stage we focus on maximizing savings for retirement, home/debt pay down begins to increase, we increase college savings for children, plan for the financial cost of caring for aging parents, and begin an estate plan. At this stage, it is vital that all insurance coverages and appropriate amounts are in place.

Pre-Retiree (Final working years, generally 5 years or less until retirement)

Pre-retirees are focused on maximum accumulation through intense, tax efficient saving. Depending on the circumstance, we may begin to adjust portfolio allocations to be prepared for retirement income. Often, in this stage, we are caring for aging parents, healthcare becomes priority, second careers are pursued and volunteer work ramps up. This is the time to begin pursuing long term care insurance to cover advanced health care costs.

Retiree and Legacy Distributor (from retirement until death)

The emphasis of this stage is stable and predictable income. Many of our clients are focusing on passing on family values, charitable giving, and leaving a lasting legacy to their family and community. By this stage, it is critical that long term care costs is planned for, estate plans are revised and updated, and income is stable.

So, what’s the big deal if we follow the herd and sell when prices are going down? Especially if it makes us feel better. We can always buy back in, right? This is what’s known as trying to “time the markets.” You sell before it declines more and buy just before it goes back up too high. While this may sound tempting, it could end up costing you money. Timing the market incorrectly can set you back significantly. If you sell when the market’s declining, you have to figure out exactly when to reenter. If you do this at the wrong time, you “lock in your loss.” This happens because you don’t know in advance what the bottom will be—and by the time you figure it out, you’re selling close to the lowest point. When you do decide to buy back in, after seeing if the market is truly starting to move upwards once again, prices have already increased.

EXAMPLE: To explain what this means, let’s imagine a scenario. Let’s say you invest $10 and the market declines, making your investment worth $5. You sell out. Now you have $5 instead of $10 dollars. A few weeks later, that same stock goes back up to $12. But because you sold out, you didn’t benefit from that increase. You’re stuck with a $5 loss. It could continue to increase, but you have a challenge. Before you can make money again, you need it to go up to $19 to make up for the $7 you lost. Then you need it to go up even higher so you can actually make money off your investment. That’s a steep hill to climb. If you’d just stayed invested, you’d have made $2 instead of lost $7. This is a simplified hypothetical example of an investing concept and is not representative of any specific investment. Your results may vary.

Once again, history tells an interesting story. The investing herd has followed our example above, and attempted to time the markets, potentially losing out on 4.7% in returns over 30 years like the average investor.* * Dalbar Inc., “Quantitative Analysis of Investor Behavior,” March 2020.

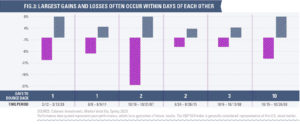

The other problem with timing the markets is that the best days—when you could potentially make the most money—tend to occur right next to the worst days.

There’s no way to know exactly when the market is going to go back up again. Something could even happen after market close one day that causes the markets to increase the next—before you have a chance to buy back in if you’ve sold out. In fact, if you started investing in 1990 and missed the S&P 500’s best day of the year each year, your annual return was nearly cut in half. The annualized return for the S&P 500 from 1990 to 2019 was 7.7%. Yet, if you missed only the best day of each year, that return dropped to only 3.9%. Miss the best two days of each year, and you were up less than 1% a year. Taking it to the extreme, if you missed the best 20 days of each year, you’d be down 27% per year.

No one can consistently pick the best or worst days of the year, which is why it can be so dangerous to attempt timing the market. If you miss one or two big days, compounded over time, this can greatly impact your portfolio. By going against the flow and staying invested in your long-term plan, you could potentially end up with returns—like the S&P 500 Index return of 9.96% since 1990*—that can help you work toward your future goals.

The word “diversification” is one of those $20 words you hear in financial news. Here’s a simple definition: To spread out your money across different kinds of investments. Think of the old proverb, “Don’t put all your eggs in one basket.” In this situation, the eggs represent your money and the basket represents mutual funds.

The easiest way to make sure your investment portfolio is diversified is by putting your money into four different mutual funds. Here are the funds you’re looking for:

Growth and Income (25%): These funds bundle stocks from larger, more established companies. These funds are the most predictable and are less prone to wild highs or lows. Typically, though, they won’t earn as much money as other funds.

Growth (25%): These funds are made up of stocks from growing companies. They often earn more money than growth and income funds but less than aggressive growth funds.

Aggressive Growth (25%): These funds have the highest risk and highest possible reward. They’re made up of stocks in companies that have high growth potential, but they’re also less established and could swing widely in value.

International (25%): These funds are made up of stocks from companies outside the U.S.

Taxes shouldn’t be the primary driver of your investment strategy—but it makes sense to take advantage of opportunities to manage, defer, and reduce taxes.

Manage federal income taxes by considering the role of losses, the timing of investments, and investment selection.

Using tax-deferred accounts when appropriate can help keep more of your money invested and working for you—and then you can pay taxes on withdrawals in the future.

Reduce taxes by considering strategies like donating appreciated securities to charity, and funding education expenses using a 529 plan.

What’s one key to success in investing? Compound interest. Yep. It’s that basic. But you need to understand that compound interest works behind the scenes for years before you can see significant growth. But then out of nowhere, you’ll see crazy growth—if you’re patient.

Let’s say you get a job at age 25 and take advantage of your company’s 401(k) plan. You’re young and your salary isn’t huge, but you put away $200 a month toward your investments.

If you did that for 40 years, you’d contribute $96,000. But you’d earn over $1 million in growth, assuming a 10% return. If you’d put away $250 instead, you’d invest $120,000 over 40 years, but you could end up with $1.3 million in growth. That’s how compound interest works.

RULE OF 72: HOW LONG IT TAKES FOR INVESTMENTS TO DOUBLE

You might have heard the term, “Rule of 72.” It’s a simple math trick you can use to figure out compound interest. You simply divide the interest rate into 72. So, at an interest rate of 10%, any money you have will take 7.2 years to double. In 7.2 years, $1,000 will become $2,000. It would take the same amount of time for $500,000 to become $1 million.

Why is this information helpful? Because you can look at your current investment portfolio and figure out how much time (roughly) it will take for that money to double. It also shows the importance of giving compound interest plenty of time to do its work. If you hang on, that $250 monthly investment could make you an everyday millionaire. Slow and steady wins the race.

We work with you to construct a plan designed to weather short-term market declines and help you work toward your goals over the long term. We aim to reach for your goals, which are certain, rather than market performance, which is uncertain. Chasing market performance could also introduce unnecessary risk, whereas pursuing your goals ensures we’re managing risk where we can and seeking to build value over the long term.

When working with us to build and evaluate your plan, we encourage you to view it in light of its long-term objectives. We anticipate and plan for market dips and spikes and keep our eye on the horizon when constructing your strategy. By keeping your view focused on the long term, you can reduce the emotional impact of short-term changes in account value. If the past has told us anything, it’s that the value will likely be different tomorrow!

We’re here to coach you through challenging market environments and help you maintain your long-term view. We’ll also look for opportunities to make adjustments as needed, and we can always revisit your goals and risk tolerance as your life and perspective changes. Together, we can make a plan for any market environment. By sticking to it, you help increase the chances of reaching your goals.

Financial Advisors Keep Your Investment Plan on Track.

Financial advisors can keep you on track in saving for retirement. In fact, a study from John Hancock showed that 70% of those who work with a financial advisor are on track or ahead in saving for retirement, compared to just 33% of those who don’t use an advisor.(10) Seventy percent is a whole lot better than 33%!

Here’s another stat that will motivate you: Fidelity surveyed its investors, and 75% of them have more confidence in the investment accounts managed by a

financial advisor than accounts they manage themselves. In comparison, those

who have a written plan prepared by a professional advisor have about $203,000 saved for retirement.(11)

Financial Advisors Do More than Invest Your Money.

Some people think that a financial advisor’s only job is to invest money. That’s one of their roles, but it’s not the only one. They can also work with you on a

wide range of other financial needs:

REBALANCING INVESTMENTS: Remember, your investing portfolio is probably made up of different kinds of investments. As that portfolio grows, you will need to rebalance the investments in it so that you have 25% in each of the four fund types I suggested. A financial advisor can work with you to make sure your funds stay balanced over time.

SPENDING STRATEGIES: When you retire, which of your investments will require a minimum withdrawal every year? Which income stream should you tap first? Questions like these are

critical when you start using the money you’ve been saving. A financial advisor can help you make the best decisions in this area.

TAX PLANNING: Do you know what tax laws apply to your financial situation? Or which investment will be taxed the most? A financial advisor will know the answers to those questions. They know which of your assets will have the most impact on your taxes, when those taxes are due, and how much will be owed. Advisors help you stay on good terms with Uncle Sam!

ESTATE PLANNING: Your financial advisor can work with an estate attorney to make sure your assets are distributed according to your instructions, instead of being controlled by some random probate court.

Financial Advisors Save You Time and Stress.

Think about your typical workday. You’re crazy busy from the time you wake up until you hit the pillow at night, aren’t you? Let me ask you an honest question: Do you really think you can put in the hours of research it takes to choose the right mutual funds and find the right balance of those funds?

Fidelity surveyed its program participants, and they said that lack of time was one reason they started working with a financial advisor.(12) Even if I had the time, I’d much rather spend it with my family. An afternoon tossing around the football with my boys is better than pouring over numbers. An advisor can save you countless hours that you just can’t get back otherwise.

Financial Advisors Keep Your Emotions in Check.

Listen to me, people: When the stock market takes a huge drop—like it did with the financial crisis of 2008—your stomach will start churning. You want to work with a financial advisor who can remind you that the market has always gone back up, and you don’t want to miss those future gains by cashing out. Otherwise, your emotions could take over your logic and cause you to make some stupid decisions—like taking out all your money and hiding it under a mattress.

That’s why you need an advisor. Feelings are real, but they don’t always tell you the truth.

Most investing professionals are paid one of two ways:

- A fee-based pro receives ongoing pay based on a percentage of the assets they manage for you. Their pay rises and falls based on how your portfolio is doing.

- A commission-based investing professional is paid up-front based on a percentage of the money you invest. That percentage varies from one investment to another.

Understanding Mutual Fund Fees:

Fees usually fall under two major umbrellas: transaction fees and ongoing fees.

TRANSACTION FEES: Unlike ongoing fees, transaction fees are one-time expenses you pay anytime someone makes a change to your investments (buys or sells mutual fund shares). These costs are also called shareholder fees or individual expenses. Here are some common charges:

- Commissions (or sales charges)

- Redemption fees (when you sell shares in a fund)

- Exchange fees (taking money out of one mutual fund and putting it in another)

- Account service fees (if your account drops below a certain amount)

The more you buy, sell, or change anything in your retirement account, the more fees you pay. And that cuts into your retirement fund.

ONGOING FEES: These are sometimes called annual operating expenses. With thousands of different funds in the mutual fund industry worldwide, these fee amounts can differ a lot, but they usually pay for services like:

- Managing the fund’s portfolio (keeping track of what you’re invested in)

- Record keeping (tracking what you’ve bought or sold; sending information for filing taxes)

- Marketing fees (also known as 12b-1 fees)

- Customer service (telephone and web)

Here's a Deeper Look into Our Services

Where will your retirement money come from? If you’re like most people, qualified-retirement plans, Social Security, and personal savings and investments are expected to play a role. Once you have estimated the amount of money you may need for retirement, a sound approach involves taking a close look at your potential retirement-income sources.

The Power of Tax-Deferred Growth

Why are 401(k) plans, annuities, and IRAs so popular?

The First Steps (Weeks 0-3)

BREATHE

Losing a spouse is one of the most stressful events that can happen to a person. A flood of emotions is likely to occur and it is easy to lose focus of the necessary financial tasks. Don’t make immediate large financial decisions, but do know the first steps that need to be completed in a relatively timely manner. Have a friend or family member help you through the process…and know that it is alright to BREATHE first.

Contact the funeral home for preparations and payment.

For a nominal fee from the funeral home, order 12-15 death certificates. Various financial institutions will require original copies of a death certificate, so it is important to have enough ahead of time.

Call your spouses’ employer, specifically their human resources department, to let them know of their passing. The human resources department should provide information and paperwork for pension disbursements, 401k rollover options, insurance disbursements or continuation, and the like.

Contact an attorney (your attorney if you have one) to discuss your spouses’ will or estate plan. There may be assets that will be probated and the attorney can discuss those details, along with paying an debt possessed by your spouse.

Additional Primary Steps (Weeks 3-8)

Notify all banks and investment institutions of your spouses’ passing and provide them with a death certificate if the accounts were in their name or as a joint account. If accounts are listed in trust name, those accounts will still require a death certificate and removal of your spouse as a trustee. It is wise to leave one joint bank account or trust account with your spouses’ name on it, as residual checks in your spouses’ name may still arrive for up to six months after passing.

Contact the Social Security Administration regarding spousal and surviving benefits. You may want to consult with your Financial Advisor and Accountant regarding the appropriate time to begin those benefits.

If applicable, contact the Veterans’ Administration to understand any benefits that may be owed on behalf of your veteran spouse.

Update any deeds or titles to property with your spouses’ name attached. This would include the title to your home, any vehicle registrations listed with the DMV, and investment property titles.

Have a plan for paying bills that may still be outstanding or in your spouses’ name. There may be some memberships, such as gym, clubs, etc., that will continue automatic payment unless they are notified and canceled. Be sure to write a list of all potential automatic payments that will continue unless canceled.

The Next Steps (Weeks 6 and beyond)

Speak to a Financial Advisor to devise a comprehensive financial plan going forward. Understand your future income and expenses, investment assets, and needed rates of return to continue to fund yours and your family’s lifestyle.

Also, just as important is to create a lifestyle plan. Discuss and devise a plan for those goals and dreams you want to accomplish in life, whether that be travel, a vacation home, or more time spent with family. Then attach a spendthrift plan to see those dreams come to fruition!

Update beneficiaries on all new and existing investment accounts, bank accounts, and insurance policies.

Talk to an accountant about what your tax situation might look like in that first year, as well as going forward with any new additional assets and income.

It is important to know the documents that will be needed during weeks following the passing of a spouse. The following list will help you through the process of settling an estate and taking care of important details. Gathering these documents will inform you of accounts that will need to have the passing spouse removed from title so as to not continue receiving unnecessary charges. Not all documents may be contained in the same location, so be sure to check bank safety deposit boxes and storage lockers.

Funeral Arrangements

Death Certificate

Tax Returns (For previous 2 years)

Social Security Cards

Mortgages

Other Outstanding Loan Documents

Deeds and/or Leases

Motor Vehicle Titles

Car Insurance Policies

Recent Bank Account Statements

Recent Investment Account Statements

Life Insurance Policies

Pension and/or Retirement Plan Statements

Homeowners’ Insurance Policies

Health Insurance Policies

All Monthly Bills

Effective estate management enables you to manage your affairs during your lifetime and control the distribution of your wealth after death. An effective estate strategy can spell out your healthcare wishes and ensure that they’re carried out – even if you are unable to communicate. It can even designate someone to manage your financial affairs should you be unable to do so.

Charitable Giving: Smart from the Heart

Do you have causes that you want to support with donations? Here are three tips.

Investing should be easy – just buy low and sell high – but most of us have trouble following that simple advice. There are principles and strategies that may enable you to put together an investment portfolio that reflects your risk tolerance, time horizon, and goals. Understanding these principles and strategies can help you avoid some of the pitfalls that snare some investors.

Bridging the Confidence Gap

In the world of finance, the effects of the “confidence gap” can be especially apparent.

Insurance transfers the financial risk of life’s events to an insurance company. A sound insurance strategy can help protect your family from the financial consequences of those events. A strategy can include personal insurance, liability insurance, and life insurance.

Extended Care: A Patchwork of Possibilities

What is your plan for health care during retirement?

Understanding tax strategies and managing your tax bill should be part of any sound financial approach. Some taxes can be deferred, and others can be managed through tax-efficient investing. With careful and consistent preparation, you may be able to manage the impact of taxes on your financial efforts.

The Facts About Income Tax

Millions faithfully file their 1040 forms each April. But some things about federal income taxes may surprise you.

One of the keys to a sound financial strategy is spending less than you take in, and then finding a way to put your excess to work. A money management approach involves creating budgets to understand and make decisions about where your money is going. It also involves knowing where you may be able to put your excess cash to work.

Surprise! You’ve Got Money!

Here’s a quick guide to checking to see if you have unclaimed money.

Creating a life map involves a close review of personal finances and an assessment of other building blocks. Lifestyle matters look at how to balance work and leisure, how to make smart choices for the future, and many other items in an effort to help an individual “enjoy the journey.”

Forecast

The market is as unpredictable as the weather. We’d love to help you prepare.

Tax Calendar

Key dates from the federal tax calendar.

January 31

Employers must send out W-2 Forms and 1099 Forms to employees and non-employees who provide services.

February 15

If you claimed exemption from income tax withholding on the W-4 Form you gave your employer last year, you must file a new Form W-4 by this date to continue your exemption for another year.

February 28

Businesses must file paper copies of Form 1099 with the Internal Revenue Service.

March 15

Businesses must file Form 1120 for the calendar year and pay any taxes due.

April 15

2018 individual income tax returns due, along with any tax, interest, and penalties due.

Last day to contribute to a traditional IRA, Roth IRA, or SEP-IRA for the 2018 tax year.

Estimated tax for the 1st quarter of 2019 due for those who do not pay their income tax throughout the year through withholding.

June 17

2018 individual income tax returns due for those who live outside the United States.

Estimated tax for the 2nd quarter of 2019 due for those who do not pay their income tax throughout the year through withholding.

September 16

Estimated tax for the 3rd quarter of 2019 due for those who do not pay their income tax throughout the year through withholding.

Business tax returns due for those businesses that were given a 6-month extension to file returns for 2018.

October 15

Individual income tax returns due for those who were given a 6-month extension to file income tax returns for 2018, along with any tax, interest, and penalties due.

C Corporations tax returns due for those businesses that were given a 6-month extension to file returns for 2018.

January 15, 2020

Estimated tax for the 4th quarter of 2019 due for those who do not pay their income tax throughout the year through withholding.

Tax Forms

These links will let you download the Internal Revenue Service’s most frequently requested tax forms. Clicking on one of these links will download a PDF version of the form directly from the Internal Revenue Service website.

1040

U.S. Individual Income Tax Return

Form | Instructions

1040A

U.S. Individual Income Tax Return

Form | Instructions

1040ES

Estimated Tax for Individuals. Estimated tax is the method used to pay tax on income that is not subject to withholding (for example, earnings from self-employment, interest, dividends, rents, or alimony).

Form & Instructions

1040EZ

U.S. Individual Income Tax Return for Single and Joint Filers with No Dependents

Form | Instructions

1040X

Amended U.S. Individual Income Tax Return

Form | Instructions

Schedule A (1040)

Itemized Deductions. If you itemize, you can deduct a part of your medical and dental expenses and un-reimbursed employee business expenses, and amounts you paid for certain taxes, interest, contributions, and miscellaneous expenses. You can also deduct certain casualty and theft losses.

Form | Instructions

Schedule B (Form 1040)

Interest and Ordinary Dividends.

Form & Instructions

Schedule C (Form 1040)

Profit or Loss from Business (Sole Proprietorship)

Form | Instructions

Schedule D (Form 1040)

Capital Gains and Losses. Use this form to report the sale or exchange of a capital asset not reported on another form or schedule, gains from involuntary conversions (other than from casualty or theft) of capital assets not held for business or profit, capital gain distributions not reported directly on Form 1040, and non-business bad debts.

Form | Instructions

Schedule M (Form 990)

Making Work Pay Credit. Use Schedule M to figure the making work pay credit. This credit may give you a refund even if you do not owe tax.

Form

Schedule SE (Form 1040)

Self-Employment Tax. Use this form to figure the tax due on net earnings from self-employment. The Social Security Administration uses the information from Schedule SE to figure your benefits under the social security program.

Form | Instructions

W-4

Employee’s Withholding Allowance Certificate. Complete this form so your employer can withhold the correct federal income tax from your pay.

Form & Instructions

W-2

Wage and Tax Statement. Every employer who pays for services performed by an employee, including noncash payments, must file a Form W-2 for each employee — even if the employee is related to the employer.

Form | Instructions

W-9

Request for Taxpayer Identification Number and Certification. Anyone who is required to file an information return with the IRS must obtain your correct taxpayer identification number (TIN) to report, for example, income paid to you, real estate transactions, mortgage interest you paid, acquisition or abandonment of secured property, cancellation of debt, or contributions you made to an IRA.

Form | Instructions

1099

Miscellaneous Income Statement. Every business that pays for services performed by a non-employee must file a copy of Form 1099 for each non-employee.

Form | Instructions

941

Employer’s Quarterly Federal Tax Return.

Form | Instructions

4868

Application for Automatic Extension of Time To File U.S. Individual Income Tax Return. Use this form to apply for 6 more months to file Form 1040, 1040A, 1040EZ, 1040NR, 1040NR-EZ, 1040-PR, or 1040-SS.

Form & Instructions

8863

Education Credits (American Opportunity and Lifetime Learning Credits). Use this form to figure and claim tax credits for qualified education expenses paid to an eligible postsecondary educational institution.

Form | Instructions

This content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.

Tax Publications

These links will let you download a number of very useful tax publications from the Internal Revenue Service. Clicking on one of these links will download a PDF version of the publication directly from the Internal Revenue Service website.

Your Rights As a Taxpayer

This publication explains some of your most important rights as a taxpayer and the examination, appeal, collection, and refund processes.

Armed Forces’ Tax Guide

This publication covers the special tax situations of active members of the U.S. Armed Forces. It does not cover military pensions or veterans’ benefits or give the basic tax rules that apply to all taxpayers.

Your Appeal Rights and How To Prepare a Protest If You Don’t Agree

This Publication tells you how to appeal your tax case if you don’t agree with the Internal Revenue Service findings in an audit or other review.

Employer’s Tax Guide

A guide to taxes for employers and business owners.

Your Income Tax for Individuals

This publication covers the general rules for filing a federal income tax return. It explains the tax law to help you make sure you pay only the tax you owe and no more.

Tax Guide for Small Businesses (for individuals who use Schedule C or Schedule C-EZ)

The publication provides general information about the federal tax laws that apply to small business owners who are sole proprietors and to statutory employees. It provides information on business income, expenses, and tax credits that may help you file your income tax return.

Exemptions, Standard Deduction, and Filing Information

This publication discusses some tax rules that affect every person who may have to file a federal income tax return. It answers some basic questions: who should file; what status to use; how many exemptions to claim; and the amount of the standard deduction.

Medical and Dental Expenses (including the Health Coverage Tax Credit)

This publication explains the itemized deduction for medical and dental expenses that you claim on Schedule A (Form 1040).

Child and Dependent Care Expenses

This publication explains the tests you must meet to claim the credit for child and dependent care expenses.

Divorced or Separated Individuals

This publication explains tax rules that apply if you are divorced or separated from your spouse.

Charitable Contributions

This publication explains how to claim a deduction for your charitable contributions.

Business Expenses

This publication discusses common business expenses and explains what is and is not deductible.

Examination of Returns, Appeal Rights, and Claims for Refund

This publication discusses general rules and procedures that the IRS follows in examinations.

Individual Retirement Arrangements (IRAs)

This publication discusses traditional, Roth, and SIMPLE IRAs. It explains the rules for setting up an IRA, contributing to an IRA, transferring money or property to or from an IRA, receiving distributions from an IRA, and taking credit for contributions to an IRA.

Survivors, Executors, and Administrators

This publication is designed to help those in charge of the estate of an individual who has died. It shows them how to complete and file federal income tax returns and explains their responsibility to pay any taxes due on behalf of the deceased person.

Health Savings Accounts and Other Tax-Favored Health Plans

This publication explains health savings accounts (HSAs), medical savings accounts (Archer MSAs and Medicare Advantage MSAs), health flexible spending arrangements (FSAs), and health reimbursement arrangements (HRAs).

This content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.

Tax Rates

Please note: Tax rates are for the 2019 tax year and will be updated to 2020 rates after April 15th of the current year.

Married Filing Jointly

| Over | Not Over | Rate |

|---|---|---|

| $0 | $19,400 | 10% |

| $19,401 | $78,950 | 12% |

| $78,951 | $168,400 | 22% |

| $168,401 | $321,450 | 24% |

| $321,451 | $408,200 | 32% |

| $408,201 | $612,350 | 35% |

| $612,351 | 37% |

Married Filing Separately

| Over | Not Over | Rate |

|---|---|---|

| $0 | $9,700 | 10% |

| $9,701 | $39,475 | 12% |

| $39,476 | $84,200 | 22% |

| $84,201 | $160,725 | 24% |

| $160,726 | $204,100 | 32% |

| $204,101 | $306,175 | 35% |

| $306,176 | 37% |

Single

| Over | Not Over | Rate |

|---|---|---|

| $0 | $9,700 | 10% |

| $9,701 | $39,475 | 12% |

| $39,476 | $84,200 | 22% |

| $84,201 | $160,725 | 24% |

| $160,726 | $204,100 | 32% |

| $204,101 | $510,300 | 35% |

| $510,301 | 37% |

Head of Household

| Over | Not Over | Rate |

|---|---|---|

| $0 | $13,850 | 10% |

| $13,851 | $52,850 | 12% |

| $52,851 | $84,200 | 22% |

| $84,201 | $160,700 | 24% |

| $160,701 | $204,100 | 32% |

| $204,101 | $510,300 | 35% |

| $510,301 | 37% |

This content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.

1035 Exchange

A method of exchanging insurance-related assets without triggering a taxable event. Cash-value life insurance policies and annuity contracts are two products that may qualify for a 1035 exchange.

401(k) Plan

A qualified retirement plan available to eligible employees of companies. 401(k) plans allow eligible employees to defer taxation on a specific percentage of their income that is to be put toward retirement savings; taxes on this deferred income and on any earnings the account generates are deferred until the funds are withdrawn—normally in retirement. Employers may match part or all of an employee’s contributions. Employees may be responsible for investment selections and enjoy the direct tax savings.

401(k) Loan

A loan taken from the assets within a 401(k) account. 401(k) loans charge interest and are normally paid back through payroll deductions. If the borrower leaves an employer before a 401(k) loan has been repaid, the full amount of the loan is generally due. If the borrower fails to repay the loan, it is considered a distribution, and ordinary income taxes may be due, along with any applicable tax penalties.

403(b) Plan

A 403(b) plan is similar to a 401(k). A 403(b) is a qualified retirement plan available to employees of non-profit and government organizations.

Account Balance

The amount held in an account at the end of a reporting period. For example, a credit card account balance would show the amount owed to a lender as a result of purchases made during a specific period.

Adjustable-Rate Mortgage (ARM)

A mortgage with an interest rate that is adjusted periodically based on an index. Adjustable-rate mortgages generally have lower initial interest rates than fixed-rate mortgages because the lender is able to transfer some of the risk to the borrower; if prevailing rates go higher, the interest rate on a variable mortgage may adjust upward as well.

Adjusted Gross Income (AGI)

One figure used in the calculation of income tax liability. AGI is determined by subtracting allowable adjustments from gross income.

Administrator

A probate-court-appointed person who is tasked with settling an estate for which there is no will.

After-Tax Return

The return on an investment after subtracting any taxes due.

Aggressive Growth Fund

A mutual fund offered by an investment company that specifically pursues substantial capital gains. Mutual fund balances are subject to fluctuation in value and market risk. Shares, when redeemed, may be worth more or less than their original cost. Mutual funds are sold only by prospectus. Individuals are encouraged to consider the charges, risks, expenses, and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully before you invest or send money.

Alternative Minimum Tax (AMT)

A method of calculating income tax with a unique set of rules for deductions and exemptions that are more restrictive than those in the traditional tax system. The AMT attempts to ensure that certain high-income taxpayers don’t pay a lower effective tax rate than everyone else. To determine whether or not the AMT applies, taxpayers must fill out IRS Form 6251.

American Stock Exchange (AMEX)

A stock exchange originally located in New York City. AMEX was taken over by NYSE Euronext—the group that operates the New York Stock Exchange—in January 2009.

Annual Percentage Rate (APR)

The yearly cost of a loan expressed as a percentage of the loan amount. The APR includes interest owed and any fees or additional costs associated with the agreement.

Annual Report

A report required by the Securities and Exchange Commission (SEC) of any company issuing registered stock, that describes a company’s management, operations, and financial reports. Annual reports are sent to shareholders, and must also be available for public review.

Annuity

A contract with an insurance company that guarantees current or future payments in exchange for a premium or series of premiums. The interest earned on an annuity contract is not taxable until the funds are paid out or withdrawn. Withdrawals and income payments are taxed as ordinary income. If a withdrawal is made prior to age 59½, penalties may apply. The guarantees of an annuity contract depend on the issuing company’s claims-paying ability. Annuities have fees and charges associated with the contract, and a surrender charge also may apply if the contract owner elects to give up the annuity before certain time-period conditions are satisfied.

Appraisal

A formal assessment of a property’s value at a specific point in time, performed by a qualified professional.

Asset

Anything owned that has a current value that may provide a future benefit.

Asset Allocation

A method of allocating funds to pursue the highest potential return at a specific level of risk. Asset allocation normally uses sophisticated mathematical analysis of the historical performance of asset classes to attempt to project future risk and return. Asset allocation is an approach to help manage investment risk. It does not guarantee against investment loss.

Asset Class

A specific category of investments that share similar characteristics and tend to behave similarly in the marketplace.

Audit

In accounting, the formal examination of a company’s financial records by a qualified professional to determine the records’ accuracy, consistency, and conformity to legal standards and established accounting principles. In taxes, the formal examination of a tax return by the Internal Revenue Service or other authority to determine its accuracy.

Automatic Reinvestment

An arrangement under which an institution automatically deposits dividends or capital gains generated by an individual’s investment back into the investment to purchase additional shares.

Balanced Mutual Fund

A mutual fund offered by an investment company which attempts to hold a balance of stocks and bonds. Mutual funds are subject to fluctuation in value and market risk. Shares, when redeemed, may be worth more or less than their original cost. Mutual funds are sold only by prospectus. Individuals are encouraged to consider the charges, risks, expenses, and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully before you invest or send money.

Bear Market

A market experiencing an extended period of declining prices. A bear market is the opposite of a bull market.

Beneficiary

The person or entity who will receive benefits from a life insurance policy, qualified retirement plan, annuity, trust, or will upon the death of an individual.

Blue Chip Stock

The stock of an established company which has a history of generating a profit and possibly a consistent dividend.

Bond

A debt instrument under which the issuer promises to pay a specified amount of interest and to repay the principal at maturity. The market value of a bond will fluctuate with changes in interest rates. As rates rise, the value of existing bonds typically falls. If an investor sells a bond before maturity, it may be worth more or less than the initial purchase price. By holding a bond to maturity, an investor will receive the interest payments due plus his or her original principal, barring default by the issuer. Investments seeking to achieve higher yields also involve a higher degree of risk.

Book Value

The value of a company’s assets minus its liabilities, preferred stock, and redeemable preferred stock.

Bull Market

A market experiencing an extended period of rising prices. A bull market is the opposite of a bear market.

Buy-and-Hold

An investment strategy that advocates holding securities for the long term and ignoring short-term price fluctuations in the market.

Buy-Sell Agreement

A legal contract that provides for the purchase of all outstanding shares from a business owner who wishes to sell, wants to terminate involvement, is permanently disabled, or has died. Buy-sell agreements are often funded with life insurance.

Capital Gain or Loss

The difference between the price at which an asset was purchased and the price for which it was sold. When the sale price is higher than the purchase price, the difference is a capital gain; when the sale price is lower than the purchase price, the difference is a capital loss.

Cash Alternatives

Assets that are most easily converted into cash and which have a very low risk of price fluctuation. For example, money market funds may be considered a cash alternative. Money held in money market funds is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Money market funds seek to preserve the value of your investment at $1.00 a share. However, it is possible to lose money by investing in a money market fund.

Cash Surrender Value

The amount a policyholder would receive when voluntarily terminating a cash-value life insurance policy before the insured event occurs or when cashing out an annuity contract before its maturity. Computation of cash surrender value is stated in the life insurance or annuity contract.

Certificate of Deposit (CD)

A deposit with a bank, thrift institution, or credit union that promises a fixed interest rate on funds deposited for a specified period of time. Bank savings accounts and CDs are FDIC insured up to $250,000 per depositor per institution and generally provide a fixed rate of return, whereas the value of money market mutual funds can fluctuate.

Charitable Lead Trust

A trust established for the benefit of a charitable organization under which the charitable organization receives payment of a specified amount (at least annually) from the trust. On the death of the grantor, remainder interest in the trust passes to his or her heirs. Using a trust involves a complex set of tax rules and regulations. Before moving forward with a trust, consider working with a professional who is familiar with the rules and regulations.

Charitable Remainder Trust

A trust established for the benefit of a charitable organization under which the grantor can designate an income beneficiary to receive payment of a specified amount—at least annually—from the trust. The grantor may also be the income beneficiary. On the death of the grantor, remainder interest in the trust passes to the charitable organization. Using a trust involves a complex set of tax rules and regulations. Before moving forward with a trust, consider working with a professional who is familiar with the rules and regulations.

Claim

A request for payment under the terms of an insurance policy.

COBRA

A federal law that requires group health plans sponsored by employers with more than 20 employees to offer terminated or retired employees the opportunity to continue their health insurance coverage for a specified period at the employees’ expense.

Coinsurance or Co-Payment

A policy provision under which an insurance company and the insured party share the total cost of covered medical services after the policy’s deductible has been met.

Commercial Paper

An unsecured, short-term debt security issued by a corporation to finance short-term liabilities. These notes are normally backed only by the issuing corporation’s promise to pay the face amount on the maturity date specified on the note, which is usually less than six months.

Common Stock

A security that represents partial ownership of a corporation. Those who hold common stock are entitled to participate in stockholder meetings, to vote for the board of directors, and may receive periodic dividends.

Community Property

State laws under which most property and debts acquired during a marriage—except for gifts or inheritances—are owned jointly by both spouses and are divided upon divorce or annulment. In the United States, nine states have community property laws: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin.

Compound Interest

A process under which interest is computed both on an account’s principal and on any gains reinvested in prior periods. This is contrasted with simple interest, in which interest is calculated only on the principal amount.

Consumer Price Index (CPI)

The U.S. government’s main measure of inflation, calculated monthly by the Department of Labor.

Convertible Term Insurance

A term life insurance policy under which the policyholder has the right to convert the policy to permanent life insurance, subject to limitations. Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Corporate Bond

A debt security issued by a corporation under which the issuer promises to make periodic interest payments and to repay the investor’s principal at maturity. The market value of a bond will fluctuate with changes in interest rates. As rates rise, the value of existing bonds typically falls. If an investor sells a bond before maturity, it may be worth more or less than the initial purchase price. By holding a bond to maturity, investors will receive the interest payments due plus their original principal, barring default by the issuer. Investments seeking to achieve higher yields also involve a higher degree of risk.

Corporation

A legal organization created under the laws of a state as a separate legal entity that has privileges and liabilities that are distinct from those of its members. Corporations are taxable entities—they are taxed separately from their members or shareholders. Corporations are able to borrow money and to make a profit separately from their members or shareholders.

Coverdell Education Savings Account (Coverdell ESA)

A tax-advantaged investment account that allows accumulation of funds to cover future education expenses, subject to limitations. Coverdell ESAs allow money to grow tax deferred and proceeds to be withdrawn tax free for qualified education expenses at a qualified institution.

Credit Score

A statistical estimation of how likely a potential borrower is to pay his or her debts and, by extension, how much credit he or she should have.

Debt

An obligation owed by one party (the debtor) to a second party (the creditor).

Debt-to-Equity Ratio

The ratio of a company’s total debt to its total shareholder equity. Some use the debt-to-equity ratio to attempt to ascertain a company’s capability to repay its creditors.

Deduction

An amount that can be subtracted from gross income before income taxes are calculated.

Deed

A legal document that confirms ownership of an asset or that confirms the passage of an interest, right, or ownership in the asset from one person or legal entity to another.

Deferred Annuity

A contract with an insurance company that guarantees a future payment or series of payments in exchange for current premiums. The interest earned on an annuity contract is not taxable until the funds are paid out or withdrawn. The guarantees of an annuity contract depend on the issuing company’s claims-paying ability. Annuities have fees and charges associated with the contract, and a surrender charge also may apply if the contract owner elects to give up the annuity before certain time-period conditions are satisfied.

Defined Benefit Plan

A retirement plan under which the benefit to a retiring employee is defined. Defined benefit plans are normally funded by employer contributions.

Defined Contribution Plan

A retirement plan under which the annual contributions made by the employer or employee are defined. Benefits may vary depending on the performance of the investments in the account.

Deflation

A reduction in the price of goods and services. Deflation is the opposite of inflation.

Dependent

A person who relies on another for his or her financial support. Within limits, those who support dependents are allowed to claim certain exemptions when filing income taxes.

Direct Rollover

The direct transfer of assets from the trustee or custodian of one qualified retirement plan or account to the trustee or custodian of another. Done correctly, direct rollovers do not trigger taxable events.

Disability Income Insurance

An insurance policy that pays a portion of the insured’s income when a specified disability makes working uncomfortable, painful, or impossible.

Diversification

An investment strategy under which capital is divided among several assets or asset classes. Diversification operates under the assumption that different assets and/or asset classes are unlikely to move in the same direction, allowing gains in one investment to offset losses in another. Diversification is an approach to help manage investment risk. It does not eliminate the risk of loss if security prices decline.

Dividend

Taxable payments made by a company to its shareholders. Some dividends are paid quarterly and others are paid monthly. Companies can adjust common share dividends at any time, pending approval by the company’s board of directors.

Dollar-Cost Averaging

An investment strategy under which a fixed dollar amount of securities is purchased at regular intervals. Under dollar-cost averaging, more shares are purchased when prices are low and fewer shares when prices rise. Keep in mind that dollar-cost averaging does not protect against a loss in a declining market or guarantee a profit in a rising market. Investors should evaluate their financial ability to continue making purchases through periods of declining and rising prices.

Dow Jones Industrial Average (DJIA)

An average calculated by summing the prices of 30 actively leading stocks on the New York Stock Exchange (NYSE) and dividing the sum by a divisor which has been adjusted to account for cases of stock splits, spinoffs, or similar structural changes. Individuals cannot invest directly in an index.

Early Withdrawal

Withdrawal of funds from an investment before its maturity date or withdrawal of funds from a tax-deferred account before the legally imposed age requirements have been satisfied. Early withdrawals may be subject to penalties.

Employee Stock Ownership Plan (ESOP)

A defined-contribution plan that provides a company’s workers with an ownership interest in the company—usually as shares of company stock.

Employer-Sponsored Retirement Plan

A retirement plan sponsored by an employer for the benefit of its employees. These typically fall into one of two types: defined-contribution plans (such as SEP IRAs, 401(k) plans and 403(b) plans) and defined-benefit plans (such as traditional pensions).

Equity

The value of real property or a business after all liabilities have been paid. A home worth $300,000 with a $200,000 mortgage would have $100,000 in equity.

Employee Retirement Income Security Act (ERISA)

A federal law that establishes the regulations under which retirement plans are governed and spells out the federal income tax regulations and effects for qualified retirement plans.

Estate Management

The preparations necessary to manage a person’s financial and healthcare matters during his or her lifetime and to effectively and economically distribute the assets within that estate upon his or her death.

Estate Tax

Federal and/or state taxes that may be levied on the assets of a deceased person upon his or her death. These taxes are paid by the deceased person’s estate rather than his or her heirs.

Exchange-Traded Funds (ETFs)

A share of an investment company that owns a block of shares selected to pursue a specific investment objective. ETFs trade like stocks and are listed on stock exchanges and sold by broker-dealers. Exchange-traded funds are sold only by prospectus. Please consider the charges, risks, expenses, and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully before you invest or send money.

Executive Bonus Plan

An executive benefit paid for by an employer.

Executor

A person named by a will or appointed by the probate court to distribute the deceased’s assets as directed by the will or, in the absence of a will, in accordance with the probate laws of the state.

Federal Income Tax Bracket

A series of income ranges within which a taxpayer’s income is taxed at a certain rate. Taxpayers pay the tax rate in a given bracket only for that portion of their overall income that falls within the bracket’s range.

Federal Reserve System (The Fed)

The United States’ central bank. The Federal Reserve System consists of a series of 12 independent banks that operate under the supervision of a seven-member, federally appointed board of governors. The Fed strives to maintain maximum employment, stable price levels, and moderate long-term interest rates. It establishes and enforces the regulations banks, savings and loans, and credit unions must follow. It also acts as a clearing house for certain financial transactions and provides banking services to the federal government.

Financial Aid

Loans, grants, scholarships, and work-study programs provided by federally and privately funded sources to enable students to attend college.

Financial Statement

A formal record of the financial activities of a business, person, or other entity. For a business, financial statements typically include a balance sheet, a profit and loss statement, and a cash flow statement.

Financial Industry Regulatory Authority (FINRA)

FINRA is an independent regulator that oversees all securities firms doing business in the U.S. FINRA seeks to protect investors by making sure the securities industry operates fairly and honestly.

First-to-Die Life Insurance

Joint life insurance taken out on the lives of two or more people that pays its death benefit when the first insured person dies.

Fixed Annuity

A contract with an insurance company that guarantees investment growth at a fixed interest rate as well as current or future payments in exchange for a premium or series of premiums. The interest earned on an annuity contract is not taxable until the funds are paid out or withdrawn. The guarantees of an annuity contract depend on the issuing company’s claims-paying ability. Annuities have fees and charges associated with the contract, and a surrender charge also may apply if the contract owner elects to give up the annuity before certain time-period conditions are satisfied.

Fixed-Rate Mortgage

A mortgage with a set interest rate that will not change over the life of the loan.

Foreclosure

The legal process under which a creditor seizes the property of a borrower who has not made timely payments on his or her debt.

Front-End Load

A sales fee paid at the time an investment is purchased. This fee is deducted from the investment—thus lowering the size of the investment.

Fundamental Analysis

A method of evaluating securities that examines financial and economic factors—such as the current finances of a company and the prevailing economic environment—to determine whether the company’s future value is accurately reflected in its current stock price.

Gift

The voluntary transfer of assets under which the giver receives no compensation and retains no interest in his or her gift.

Gift Tax

A tax the federal government and some states levy on the transfer of property as a gift. Generally gift taxes increase with the amount of the gift and are paid by the donor.

Gross Monthly Income

Total monthly income generated from all sources before taxes and other expenses are considered.

Group Life Insurance

Life insurance that insures all the members of a specific group, most often the employees of a specific company or the members of a professional association.

Health Savings Account (HSA)

An account that offers individuals covered by high-deductible health plans a tax-advantaged means to save for medical expenses. Within certain limits, funds contributed to the account are not subject to federal income taxes. Unlike Flexible Spending Accounts (FSAs), funds can be rolled over from year to year if not spent.

Home Equity

The real value of a home after all liabilities have been paid. Thus a home worth $300,000 with a $200,000 mortgage would have $100,000 in equity.

Income

Monies or other compensation received from any source. This includes wages, commissions, bonuses, Social Security and other retirement benefits, unemployment compensation, disability, interest, and dividends. Generally, all income is taxable unless it is specifically exempted by law.

Index

An average of the prices of a hypothetical basket of securities representing a particular market or portion of a market. Among the most well known are the Dow Jones Industrials Index, or the Dow; the Standard & Poor’s 500 Index, or the S&P 500; and the Russell 2000 Index. Index performance is not indicative of the past performance of a particular investment. Past performance does not guarantee future results. Individuals cannot invest directly in an index.

Individual Retirement Account (IRA)

A qualified retirement account for individuals. Contributions to a Traditional IRA may be fully or partially deductible, depending on your individual circumstance. Distributions from Traditional IRA and most other employer-sponsored retirement plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70½, you must begin taking required minimum distributions.

Inflation

An upward movement in the average level of prices. Each month, the Bureau of Labor Statistics reports on the average level of prices when it releases the Consumer Price Index (CPI).

Initial Public Offering (IPO)

A company’s first public offering of stock. In an IPO, investment banks buy a company’s shares and then offer them to the public at an offering price. As the stock is traded, the market price may be more or less than the offering price. Keep in mind that the return and principal value of stock prices will fluctuate as market conditions change. And shares, when sold, may be worth more or less than their original cost.

Interest Rate

The cost to borrow money expressed as a percentage of the loan amount over one year.

Intestate

The condition of an estate when its owner dies without leaving a valid will. In such circumstances, state law normally determines who inherits property and who serves as guardian for any minor children.

Investment Objective

The stated financial goal of an investment.

Irrevocable Trust

A trust that cannot be altered, stopped, or canceled after its creation without the permission of the beneficiary or trustee. Using a trust involves a complex set of tax rules and regulations. Before moving forward with a trust, consider working with a professional who is familiar with the rules and regulations.

Joint Tenancy

A form of property ownership under which two or more people have an undivided interest in the property and in which the survivor or survivors automatically assume ownership of the interest of any joint tenant who dies.

Jointly Held Property

Property owned simultaneously by more than one person. All co-owners have an equal right to use the property, and no co-owner can exclude another co-owner from the property. The most common forms of jointly-held property are joint tenancy, tenancy in common, and, in some states, community property.

Keogh Plan

A tax-deferred retirement plan for self-employed individuals and employees of unincorporated businesses. Keogh plans are similar to IRAs but have significantly higher contribution limits. Distributions from Keogh plans and most other employer-sponsored retirement plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70½, you must begin taking required minimum distributions.

Key Employee

An employee who has valuable skills, knowledge, or organizational abilities, who is considered critical to the success of a given company.

Key Person Insurance

Company-owned insurance designed to cover the cost of replacing a key employee if he or she were to die or become disabled.

Life Insurance

A contract under which an insurance company promises, in exchange for premiums, to pay a set benefit when the policyholder dies. Several factors will affect the cost and availability of life insurance, including age, health and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Liquidity

The ease and speed with which an asset or security can be bought or sold.

Living Trust

A trust created by a living person which allows that person to control the assets he or she contributes to the trust during his or her lifetime and to direct their disposition upon his or her death.

Living Will

A written document that allows the originator to designate someone to make medical decisions on his or her behalf in the event that he or she becomes incapacitated due to accident or illness.

Long-Term-Care Insurance

Insurance that covers the cost of medical and non-medical services needed by those who have a chronic illness or disability—most commonly associated with aging. Long-term-care insurance can cover the cost of nursing home care, in-home assistance, assisted living, and adult day care.

Lump-Sum Distribution

A one-time payment of the entire amount held in an employer-sponsored retirement, pension plan, annuity, or similar account, rather than breaking payments into smaller installments.

Management Fee

The cost of having assets professionally managed. This fee is normally a fixed percentage of the fund’s asset value; terms of the fee are disclosed in the prospectus.

Marital Deduction

A provision of the tax code that allows an individual to transfer an unlimited amount of assets to his or her spouse at any time—including upon the individual’s death—without triggering a tax liability.

Market Risk

The risk that an entire market will decline, reducing the value of the investments in it without regard to other factors. This is also known as Systemic Risk.

Market Timing

An investment philosophy under which investors buy and sell securities in an attempt to profit from short-term price fluctuations.

Maturity

The date on which a debt security comes due for payment and on which an investor’s principal is due to be repaid.

Medicaid

The federal government’s health program for eligible individuals and families with low income and resources. It is means tested, meaning those who apply for benefits must demonstrate they have need.

Medicare

The federal government’s health program for individuals aged 65 and over and for individuals who have certain disabilities or end-stage renal disease.

Money Market Fund

A mutual fund that invests in assets that are easily converted into cash and which have a low risk of price fluctuation. This may include money market holdings, Treasury bills, and commercial paper. Money held in money market funds is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Money market funds seek to preserve the value of your investment at $1.00 a share. However, it is possible to lose money by investing in a money market fund.

Municipal Bond

A debt security issued by a state, county, city, or other political entity (such as a school district) to raise public funds for special projects. The income from municipal bonds is normally exempt from federal income taxes. It may also be exempt from state income taxes in the state in which the municipal bond is issued. Bond prices rise and fall daily. Municipal bonds are subject to a variety of risks, including adjustments in interest rates, call risk, market conditions, and default risk. Some municipal bonds may be subject to the federal alternative minimum tax. When interest rates rise, bond prices generally will fall. Certain municipal bonds may be difficult to sell. A municipal bond issuer may be unable to make interest or principal payments, which may lead to the issuer defaulting on the bond. If this occurs, the municipal bond may have little or no value. If a bond is purchased at a premium, it may result in realized losses. It’s possible that the interest on a municipal bond may be determined to be taxable after purchase.

Municipal Bond Fund

A mutual fund offered by an investment company which specifically invests in municipal bonds. Mutual fund balances are subject to fluctuation in value and market risk. Shares, when redeemed, may be worth more or less than their original cost. Mutual funds are sold only by prospectus. Individuals are encouraged to consider the charges, risks, expenses, and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully before you invest or send money.

Mutual Fund

A pooled investment account offered by an investment company. Mutual funds pool the monies of many investors and then invest the money to pursue the fund’s stated objectives. The resulting portfolio of investments is managed by the investment company. Mutual fund balances are subject to fluctuation in value and market risk. Shares, when redeemed, may be worth more or less than their original cost. Mutual funds are sold only by prospectus. Individuals are encouraged to consider the charges, risks, expenses, and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully before you invest or send money.

National Association of Securities Dealers Automated Quotations (NASDAQ)

An American stock exchange originally founded by the National Association of Securities Dealers. When the NASDAQ stock exchange began trading on February 8, 1971, it was the world’s first electronic stock market.

Net Asset Value

The net market value of a mutual fund’s current holdings divided by the number of outstanding shares. The product of this division estimates the per-share value of the fund’s assets.

Net Income

A company’s total revenues minus its costs, expenses, and taxes. Net income is the bottom line of a company’s income statement (which may also be called the profit and loss statement).

Net Worth

The value of a company’s or individual’s assets minus liabilities.

New York Stock Exchange (NYSE)

A stock exchange located on Wall Street in New York City, NY. Many regard the NYSE as the largest exchange in the U.S., and possibly in the world.

Non-contributory Retirement Plan

A retirement plan that is funded entirely by employer contributions, with no employee contributions.

Non-qualified Plan

A retirement or employee benefit plan that is not eligible for favorable tax treatment.

Old-Age, Survivors, and Disability Insurance (OASDI)

The official name of the Social Security program. In addition to retirement benefits, it offers disability income, veterans’ pensions, public housing, and food stamps.

Partnership

A contract under which two or more individuals manage and operate a business venture.

Permanent Life Insurance

A class of life insurance policies that do not expire—as long as premiums are kept current—and which combine a death benefit with a savings component. This savings portion can accumulate a cash value against which the policy owner may be able to borrow funds. Several factors will affect the cost and availability of life insurance, including age, health and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Policy Loan

A loan made by an insurance company to a policyholder. Policy loans are secured by the cash value of a life insurance policy. Withdrawals of earnings are fully taxable at ordinary income tax rates. If you are under age 59½ when you make the withdrawal, you may also be subject to a 10% federal income tax penalty. Also, withdrawals may reduce the benefits and value of the contract.

Policy Rider

A provision to a life insurance policy that is purchased separately from the basic policy and that provides additional benefits at additional cost.

Policyholder

The person or entity who holds an insurance policy; usually the client in whose name an insurance policy is written.

Portfolio

The combined investments of an individual investor or mutual fund.

Power of Attorney

A legal document that grants one person authority to act for another person in specific legal or financial matters in the event that said individual becomes incapacitated.

Preferred Stock

Securities that represent ownership in a corporation and have a higher claim on a company’s assets and earnings than common stock. Dividends on preferred stock are generally paid out before dividends to common stockholders.

Prenuptial Agreement

A contract entered into by those contemplating marriage that sets forth how their individual property will be divided should they ultimately divorce.

Price/Earnings Ratio (P/E Ratio)

A ratio calculated by dividing a stock’s price by its earnings per share. Investors use this ratio to learn how much they are paying for a company’s earnings.

Prime Interest Rate

The interest rate commercial banks charge their most credit-worthy or “prime” customers. The prime interest rate is influenced by the federal funds rate.

Principal

The original amount invested in a security, excluding earnings; the face value of a bond; or the remaining amount owed on a loan, separate from interest.

Probate

The court-supervised process in which a deceased person’s debts are paid and any remaining assets distributed to his or her heirs.

Property

Anything over which a person or business has legal title. Property may be held in common or privately owned.

Profit-Sharing Plan

A defined-contribution plan under which employees share in company profits. The funds within the plan accumulate tax deferred.

Prospectus

A legal document that provides the information an investor needs to make an informed decision about an investment offered for sale to the public. Prospectuses are required by and filed with the Securities and Exchange Commission.

Qualified Retirement Plan

A retirement plan that is established and operates within the rules laid down in Section 401(a) of the Internal Revenue Code, and thus receives favorable tax treatment.

Rate of Return

A measure of the performance of an investment. Rate of return is calculated by dividing any gain or loss by an investment’s initial cost. Rates of return usually account for any income received from the investment in addition to any realized capital gains.

Real Estate Investment Trust (REIT)